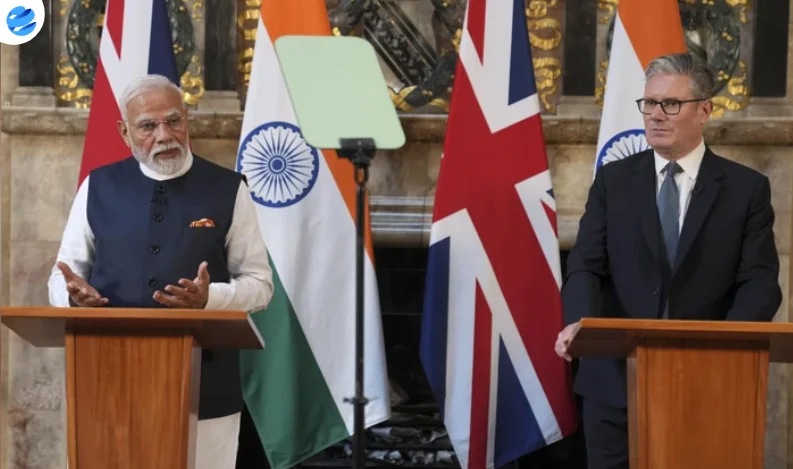

The newly signed India–United Kingdom Comprehensive Economic and Trade Agreement (CETA) is expected to catalyze a fresh wave of foreign direct investment into India, according to government officials and industry observers. Signed in London on Thursday, July 24, by Union Commerce Minister Piyush Goyal and UK Secretary of State for Business and Trade Jonathan Reynolds, the deal offers Indian goods duty-free access to the British market, provided they are manufactured locally.

The pact, which includes a detailed chapter on ‘Rules of Origin,’ outlines the criteria goods must meet to qualify for reduced tariffs under the agreement. Central to this is the provision that only goods produced within India will enjoy tariff benefits, a clause that analysts say could become a significant draw for foreign investors seeking access to UK markets.

Officials close to the negotiations said the emphasis on local sourcing would encourage multinational companies to establish or expand manufacturing operations in India. “This is not just a trade agreement; it’s a strategic move to position India as a global manufacturing hub,” one senior trade official noted.

The rules are designed to prevent companies from re-routing goods from other countries through India to benefit from lower tariffs. By tying tariff reductions to genuine domestic production, the agreement aims to create real economic incentives for both exports and job creation within India.

Several investment analysts said that global manufacturers, particularly in sectors like textiles, auto components, electronics, and pharmaceuticals, will now find India more attractive as a production base. “The FTA essentially provides a preferential corridor to the UK market, but only if companies manufacture here. That’s a compelling reason for global players to put capital into India,” said a senior analyst at a leading investment firm.

Industry groups have largely welcomed the agreement. The Confederation of Indian Industry (CII) released a statement calling the deal “a breakthrough” for India’s global trade integration, while the Federation of Indian Export Organisations (FIEO) said it would provide Indian exporters a level playing field in one of the world’s most competitive markets.

In addition to tariff reductions, CETA covers regulatory cooperation, investment facilitation, and digital trade, making it one of the most comprehensive bilateral trade agreements India has entered into in recent years. The agreement is also expected to improve India’s standing in global trade negotiations, as it joins a select group of nations with preferential access to the UK market under modern trade terms.

Government sources confirmed that the full text of the agreement will be tabled in Parliament during the upcoming monsoon session. Meanwhile, stakeholders are already gearing up to align operations and supply chains to meet the eligibility norms laid out in the pact.

With implementation expected later this year, officials said the immediate next steps will involve setting up joint committees and mechanisms to streamline customs procedures and resolve trade disputes swiftly. Business chambers have also urged the government to launch outreach programs to help small and medium exporters understand and benefit from the new trade rules.

The India–UK CETA marks a significant milestone in India’s evolving trade policy and is being positioned as a key pillar of its broader ‘Make in India’ and export-led growth strategy. With preferential market access, investor safeguards, and strict sourcing norms, the agreement could reshape India’s trade and investment landscape in the coming years.